Future portfolio performance

Long-Term Capital Market Expectations

"Prediction is very difficult, especially if it's about the future" Nobel Prize-winning physicist Niels Bohr wrote.

The future is always full of uncertainty. Our current investing environment is very challenging. This newsletter talks about the best guesses of many experts for future returns over a 10 year projection period. They have deeply researched proprietary process that draws on quantitative, qualitative inputs, valuation measures, historical risk premiums, analyst expectations, economic growth and inflation prospects. These assumptions form a critical foundation of the BFM framework for helping our clients' specific investment needs.

Our investment outlook is one of higher risks and lower returns since valuations (CAPE ratio) are high for some assets, and yields are low. Investors need to remain disciplined and globally diversified with realistic return expectations to help calibrate an appropriate savings rate for a comfortable retirement. Long-term focus, disciplined asset allocation, and periodic portfolio rebalancing will more crucial than ever before.

Even though emerging markets stocks went up 37% in 2017, the highest expected performance is for emerging markets stocks (excluding private equity) but it also has the highest expected volatility. The lowest is for government bonds.

The expected returns for the next 10 years for a simple 60/40 portfolio (60% stocks and 40% in bonds) are lower than last year. For most experts, the current expected return is between 3% to 6% compared to the extraordinary 9.5% return since 1970 and 7.4% since 1990. For stocks, most forecasts are between 2.5% (U.S.) and 9.5% (Emerging Markets). For bonds, forecasts are between 0.3% (International Treasuries) and 8.3% (Emerging Markets Debt).

Vanguard believes there is a 5% chance that the returns of a 60/40 portfolio may be below 1.3% (but also a 5% chance they may be above 7.8%). One of the most pessimistic views were from GMO's 7-year forecasts. They expect U.S. large cap stocks annualized real returns (after inflation) to be (-)4.2% while U.S. bonds would be at (-)0.5%.

After inflation (2.15% expected), the real returns (before taxes) of a 60/40 portfolio are between 1% and 4% for most experts.

If you are interested in more details and would like to have an estimate for your current portfolio, check out the Research Affiliates interactive tool. They currently forecasts that a 60/40 portfolio real return (adjusted for inflation but before tax) is 0.6%.

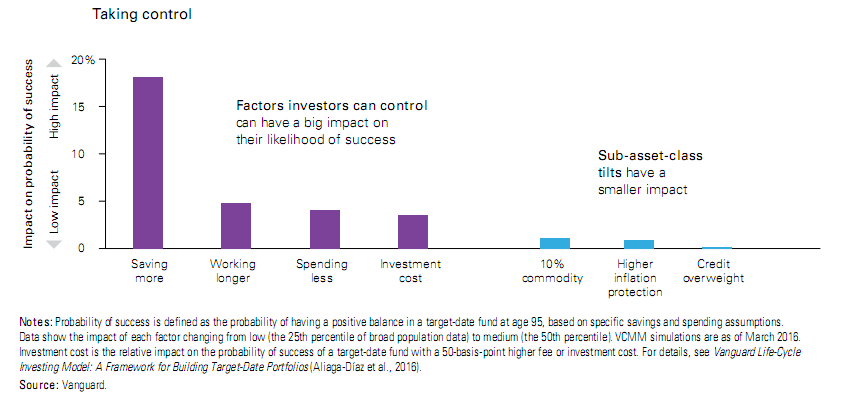

Investment success is within the control of long-term investors. Saving more is much more important than less reliable benefits of ad hoc asset-class tilts as you can see below.

Note that our newsletter is based on the 2017-2018 research of the following investment firms: Aon, AQR, BlackRock, BNY Mellon, Callan, CliffWater, Columbia Threadneedle, Franklin Templeton, JP Morgan, Merrill Lynch, Research Affiliates, Sellwood, Vanguard, Voya, and William Blair.

At BFM, we help you make better financial decisions so that you can have peace of mind.

Our core beliefs are:

• Asset Allocation is the most important determinant of performance

• A globally diversified portfolio reduces risk

• A disciplined investment process is critical

BFM enables you to increase your wealth through independent financial advice with no conflict of interest. We neither sell products nor receive commissions.

This newsletter was first published in September of 2018

https://mailchi.mp/bourbonfm/performance-1189429?e=d68f9c2d38